Engagement Feature Articles

Roundtable Discussion - Overcoming the Challenges of Capital Markets and Enhancing Corporate Value: Top Executives Discuss the Future of Dialogue with Institutional Investors

- ・Genya Takeda, Representative Director, President and COO, Sanoh Industrial Co., Ltd.

- ・Atsushi Yamaguchi, President and Representative Director, Executive Officer, Mitsubishi Steel Mfg. Co., Ltd.

- ・Hiroyasu Koike, CEO and President, Nomura Asset Management Co., Ltd.

- ・Masaki Kozue, President and Representative Director, Arr Planner Co., Ltd.

- ・Mitsuo Sugimoto, President and CEO, WILLs Inc.

As the government advances its initiative to promote "Japan as a Leading Asset Management Center" and revitalizing the capital markets becomes an urgent priority, institutional investors are increasingly being called upon to help drive corporate value creation through engagement. At the same time, companies, particularly small- and mid-cap names and those in certain sectors, have voiced concerns that opportunities to engage with institutional investors remain limited.

Against this backdrop, Nomura Asset Management hosted a roundtable discussion on February 2, 2026, with Hiroyasu Koike, President and CEO, serving as host and welcoming senior executives from four listed companies across the Growth and Prime markets. The discussion brought together top management from different companies to exchange views on a range of topics, from the structural challenges facing the capital markets to the role of IR activities in helping address them.

Please note: Titles and positions are shown as of the date of the discussion.

"CEO Engagement" and the Challenges of the Capital Markets

Koike Thank you all for joining us today. With the growing attention on the asset management industry in recent years, the role of institutional investors and the way engagement should be conducted are being scrutinized more closely than ever. At the core of the government’s "Policy Plan for Promoting Japan as a Leading Asset Management Center" is the idea that institutional investors should engage in constructive dialogue with the management of listed companies, help drive higher corporate value, in other words, greater market capitalization, and ultimately create a virtuous cycle in which those returns are passed on to the public, the final investors.

Under the banner of Project BRIDGE, we have been working to narrow the gap between market valuation and the true strength of Japanese companies through engagement activities. As part of that effort, we have also been continuing our CEO engagement initiative. I personally speak directly with CEOs of operating companies about their business strategies, capital allocation policies, views on share price, and related topics, and then share those discussions on our website, all to raise the quality of engagement.

At the same time, as a member of the Council of Experts Concerning the Follow-up of Market Restructuring, I have been taking part in those discussions, and one issue stands out very clearly to me. That is the fact that many companies working to eliminate price to book ratios below one, as well as many growth companies listed on the Growth Market, feel they have limited opportunities to engage with institutional investors. On the institutional investor side as well, there are lingering reasons not to invest, for example, the view that the Growth Market lacks liquidity.

That said, revitalizing Japan’s stock market and helping companies like yours grow and increase their market capitalization is essential for the Japanese economy. How can we chart a path forward? If we try to answer that on our own, the solution will only be so limited. Today, I would like to hear your candid views, identify the key issues together, and share those insights more broadly with society.

To begin, could you please introduce your respective companies?

Reinventing the Housing Industry through Design and Technology

Kozue I am Kozue from Arr Planner Co., Ltd. We are a housing and real estate company headquartered in Nagoya, and we have also expanded into Tokyo. We went public in February 2021, and it has now been five years since our listing. At the heart of our business is the idea of "ALL SATISFACTION," in other words, delivering satisfaction to everyone through housing.

Both our chairman and I came from major house builders, and we launched this company in order to do what we could not realize there. Many large players have shifted toward the affluent segment, but we aim to provide the public with homes that offer the same high level of design and performance as those of major house builders, at roughly 30 percent lower prices.

We have three core strengths. First, we offer strong product appeal, with homes that strike a balance between design, performance, and price, delivering excellent value for money. Second, we have strong customer acquisition capabilities through digital marketing. By leveraging video marketing on social media platforms such as Instagram and TikTok, about 80 percent of our inquiries come through the web. Third, we have strong sales capabilities as a platform that can provide custom homes, built for sale homes, and land information all in one place.

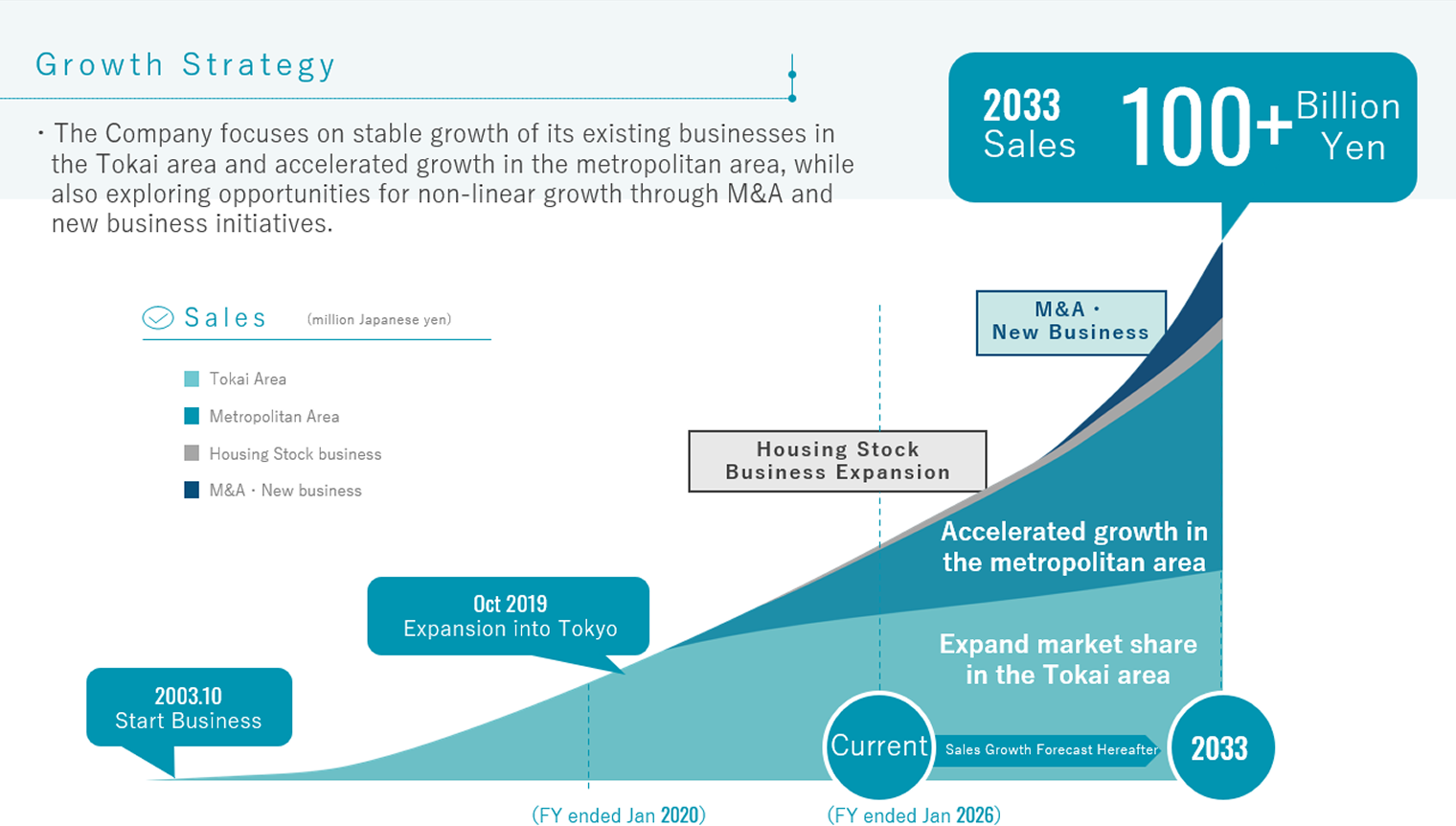

The core of our growth strategy is accelerating our business in the Tokyo metropolitan area. The detached housing market in the greater Tokyo area is extremely large, and by introducing our high-quality products particularly into the built for sale housing segment, we aim to achieve further growth. By 2033, we have set ambitious goals of reaching 100 billion yen in sales, taking on the Prime Market, and achieving a market capitalization of 100 billion yen as well.

An IR Platform That Supports the Maximization of Corporate Value

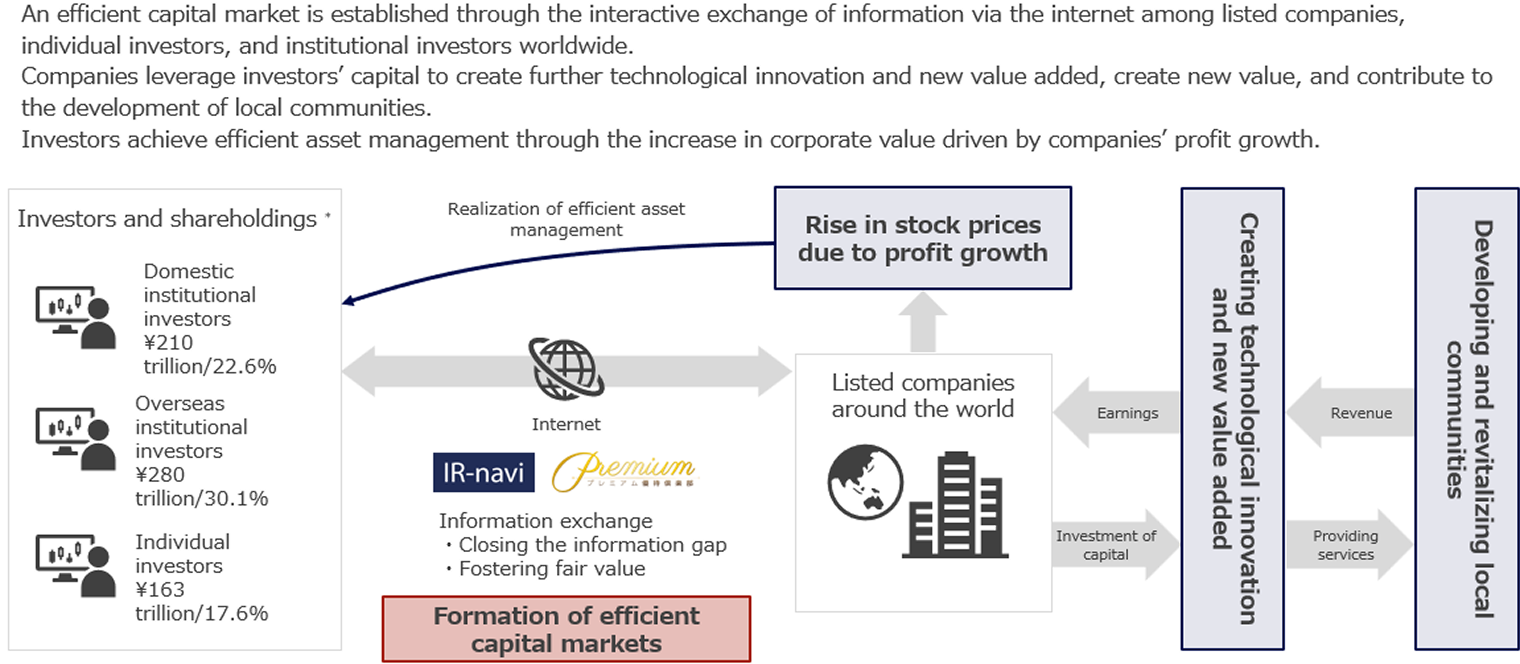

Sugimoto I am Sugimoto from WILLs. Since our founding, our philosophy has been "MAXIMIZE CORPORATE VALUE." By this, we mean not our own corporate value, but the value of our client listed companies, in other words, the maximization of their market capitalization. At present, we work with approximately 500 listed companies.

We believe that the key to enhancing corporate value lies in the shareholder portfolio. Domestic institutional investors, overseas institutional investors, and individual investors, how effectively a company markets itself to these three investor groups and builds a strong shareholder base is critical. Our concept is to support that engagement digitally over the internet and bring about a communications revolution in the capital markets.

Our business has three main pillars. The first is Premium Yutai Club, which strengthens engagement with individual investors. It is a platform that provides shareholder benefits in the form of digital points, and it is currently used by around 110 companies, with the aim of improving liquidity and supporting share price performance. More recently, it has been adopted by major airlines and food companies to digitalize engagement with hundreds of thousands of individual shareholders.

The second is IR Navi, which connects institutional investors and issuers. It includes a database of roughly 100,000 fund managers and analysts in Japan and overseas, and is used by companies, including major electronics manufacturers, that conduct IR on a global basis.

The third is our Sustainability Solutions business, which handles the production of integrated reports and related services. As non-financial disclosure becomes increasingly important, we maintain one of the leading market shares in Japan.

*Calculated by WILLs Inc. based on the results of the Tokyo Stock Exchange FY 2022 Stock Distribution Survey

Transforming a 120-Year-Old [Monozukuri] Company

Yamaguchi I am Yamaguchi from Mitsubishi Steel. Our company was founded in 1904 as Japan’s oldest spring manufacturer, and this year marks more than 120 years since our establishment. At the time, we had no choice but to rely on imports from Sweden for spring materials, and our origin lies in the spirit of "if it does not exist, let us make it ourselves," which led us to launch our special steel business.

These two businesses, springs and special steel products, form the foundation of our company, and they account for 140 billion yen out of our approximately 170 billion yen in sales. However, as you know, the steel materials business has long faced the challenge of highly volatile earnings due to sharp fluctuations in market conditions. Our spring business, too, has struggled with overseas expansion as we pursued globalization. In recent years, we have introduced ROIC based management and have been restructuring our business portfolio, including withdrawing from low margin operations.

At the same time, we are also focusing on our strategic businesses, which will drive future growth. These include precision spring application products, the materials business that produces metal powders used in 3D printers and inductors for smartphones, and our machinery business. Within the machinery business, orders have been strong in offshore wind power, defense related fields, and recycling related areas, and we are also moving forward with plans to build a new domestic plant for the first time in 30 years.

By stabilizing the profitability of our core businesses while increasing the share of profits from these strategic businesses, we aim to reduce earnings volatility and achieve sustainable growth.

From Automotive Parts to Data Centers, A Third Founding

Takeda I am Takeda from Sanoh Industrial. Our company is an automotive parts manufacturer founded in 1939. At the time of our establishment, we were mainly producing parts for fighter aircraft. After World War II, while exploring various business opportunities, we developed our pipe manufacturing technology and entered the automotive industry in the 1960s.

Today, our core products are fuel and brake pipes that run beneath the floor and through the engine compartment of vehicles, and we estimate that our global market share ranks second. In fact, one out of every four to five cars on the road worldwide is equipped with our products.

One of our defining characteristics is that we are an independent company, not part of a major automaker group. As a result, we do business not only with Japanese automakers, but also with German manufacturers and Detroit based U.S. automakers, among others. Because of the nature of our products, transportation efficiency is poor, so we have established operations near our customers’ factories and have expanded globally with a customer close business model.

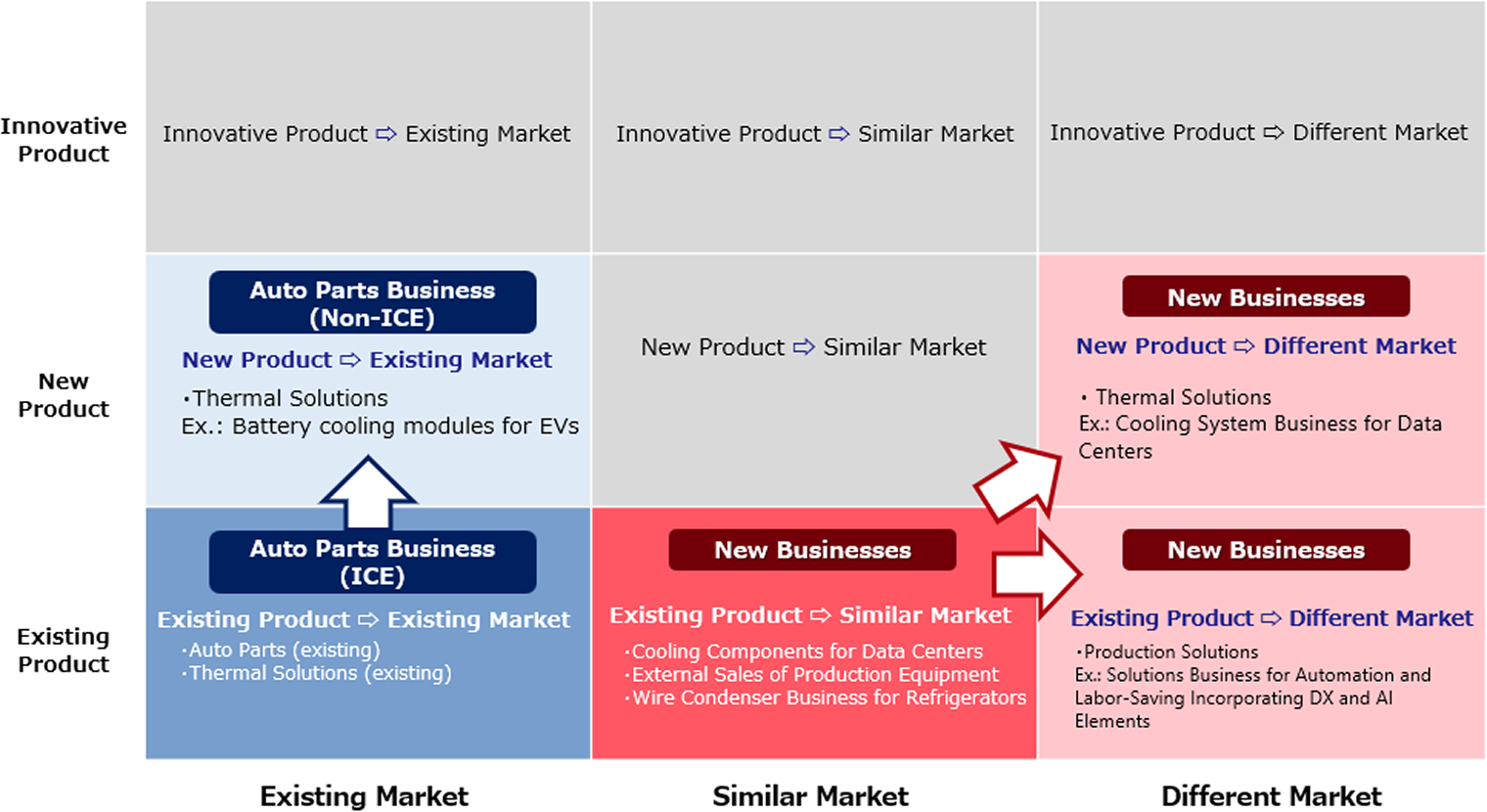

In 2021, we announced our Medium-term Strategy and Target and set forth two transformations toward what we call our "third founding." The first is a shift in our business portfolio, from existing businesses to new businesses. We aim to reduce our dependence on the automotive parts business, which currently accounts for most of our sales, and increase the share of new businesses to just over 20 percent by fiscal 2030. The second is a transformation within our existing business, from internal combustion engines to non-internal combustion engines. We will increase the share of products for non-internal combustion applications, such as thermal management products for cooling EV batteries and motors, while moving away from products tied to gasoline and other internal combustion engines.

One of the new business pillars we are focusing on is cooling systems for AI data centers. Building on our track record of developing the cooling system for the Fugaku supercomputer, we are working to expand sales to data center operators in Japan and overseas. Leveraging the leak proof technology and quality assurance capabilities we have cultivated in the automotive industry, we are aiming to create a new growth trajectory.

The Challenges of the Growth Market, Low PER and the Distance from Institutional Investors

Koike Thank you. That gives us a very clear picture of each company’s unique initiatives. From here, I would like to ask about the challenges you face in your day-to-day business. To begin with, I would like to hear about the two companies listed on the Growth Market. President Kozue, do you have any concerns regarding share prices, IR, or communication with institutional investors?

Kozue Recently our performance has recovered in a V shaped manner, and our share price has also been rising. However, one long standing challenge has been that our PER remains low compared with the average for the housing and real estate industry. It has consistently stayed in the 6 to 7 times range, while the average PER for real estate companies on the Growth Market is close to 15.

We are actively carrying out IR activities for individual investors, but the reason our PER has not expanded may be due not only to being on the Growth Market, but also to a preconceived notion among investors that the housing and real estate sector itself is undervalued.

In particular, the question is how we can increase contact with institutional investors. At present, we only hold one on one meetings when they request us, but I would welcome opportunities to approach them more proactively. After all, I believe institutional investors are the ones who move share prices. Raising our visibility and increasing opportunities for dialogue are urgent priorities for us.

Koike From what I have heard about your business, it seems you are in a very interesting position, as inflation and price increases by major house builders are driving demand toward consumers looking for more affordable housing, which is effectively flowing into your market. If that growth story is clearly communicated, I believe the market’s perception of your company could change as well.

Kozue Institutional investors have also told us that our story is interesting, but we need more opportunities to engage with a wider range of people. As for our goal of reaching a market capitalization of 100 billion yen, we believe we need to build out the underlying logic and process clearly and communicate it externally so that we can earn the market’s support and recognition.

Koike President Sugimoto, how about you? From your position supporting companies, I imagine you can take a broad view of the challenges facing both your own company and the Growth Market as a whole.

Sugimoto Speaking for our own company, we are, if you will, like the shoemaker’s children who go barefoot, and we have not been actively pursuing IR activities for institutional investors. The reason is that, given our current market capitalization and liquidity, I believe it would be a waste of time to carry out IR aimed at institutional investors.

From a macro perspective, the challenge facing the Growth Market is that structural issues are deeply rooted. For example, of the 2,000 domestic public mutual funds registered in our IR Navi database, there are only about 100 to 200 small and mid-cap funds, if that. In a market where 80 percent of Growth Market companies have a market capitalization of less than 10 billion yen, there is simply not enough capital flowing in from institutional investors. Unless that structure changes, it is extremely difficult for Growth Market companies to receive proper recognition.

That means the only segment we can realistically approach is individual investors. And what resonates most strongly with individual investors is, ultimately, hard cash, in other words, yield. In that sense, it is only natural that money from individual investors flows into foreign stocks offering yields of 4 or 5 percent, rather than Japanese stocks whose average dividend yield is around 2 percent. Our Premium Yutai Club is a mechanism designed to stimulate buying by individual investors by creating higher overall yield through shareholder benefits in addition to dividends.

I understand that the essence of IR lies in helping investors understand the business itself, but I believe this is the practical option available to many small and mid-sized companies today.

Is a "Move to the Prime Market" a Realistic Option?

Koike The reality is not that institutional investors choose not to invest in the Growth Market, but rather that they cannot. We have a fiduciary duty to our asset owners, and unless there is a compelling rationale that can support sufficient liquidity, we cannot invest the important capital entrusted to us.

We share the sense of urgency that unless this bottleneck is resolved, there is no future for Japan’s stock market. In that context, for executives of Growth Market companies, does aiming for the Prime Market become one of the key objectives?

Kozue Yes, I think so. The image of "Prime equals the former TSE First Section" remains very strong, and we have also experienced situations where the Nikkei average rises while only the Growth Index falls. So, I do see the Prime Market as offering various benefits.

Sugimoto Of the roughly 600 companies listed on the Growth Market, only about 30 have a market capitalization exceeding 50 billion yen. For a company to keep growing within the Growth Market and steadily increase its market capitalization, it would need performance strong enough for EPS, earnings per share, to continue growing exponentially. Rather than trying to clear up that very high hurdle, I believe aiming to move to the Prime Market under the current rules is the more realistic strategy.

If a company makes it to the Prime Market, it can also attract buying through index funds, which should help lift its market capitalization.

Koike Despite the Growth Market’s own concept of companies continuing to grow while remaining listed there, Prime Market migration appears more attractive from the perspective of listed companies. That, too, is one of the realities facing the Growth Market.

The Prime Market’s Challenges, PBR Below One and Remaining in TOPIX

Koike Next, I would like to hear from the two companies listed on the Prime Market. Mitsubishi Steel has been strongly emphasizing management with an awareness of capital costs and share price. President Yamaguchi, how do you view the current challenges?

Yamaguchi I believe that achieving a PBR above one is a minimum responsibility for any listed company. When we first set out this target, our PBR was around 0.5 times, so we shifted to ROIC based management to focus all our efforts on this goal.

However, our biggest recent challenge is remaining in TOPIX. I have to say that the situation is extremely difficult. To achieve that, we need to deliver a stable ROE of more than 8 percent. The major obstacle is that our core domestic steel materials business has highly volatile earnings due to factors such as demand fluctuations and intensifying international competition.

For that reason, in our current medium term management plan, we have focused on increasing the profit contribution of our strategic businesses outside the core business, such as precision springs, metal powders, and machinery. In fact, the profits from our strategic businesses have already surpassed those of our core businesses.

In the next medium term management plan, which begins in fiscal 2026, we will work to strengthen profitability and reduce uncertainty surrounding the company. By developing our strategic businesses, we need to establish key operations that will support the future, and in particular build a resilient earnings base that does not rely solely on the domestic steel materials business, which is highly sensitive to the business cycle. We want to accelerate our business portfolio reform further and connect it to higher corporate value.

That said, we are also facing the challenge that opportunities to engage with institutional investors have not increased. It may be that our name recognition and market capitalization are not yet sufficient for them to view us as an attractive investment opportunity.

Koike Looking at your disclosure materials, I see that you provide very detailed information, including ROIC and analysis of your business portfolio. How have investors been responding to such?

Yamaguchi Through our dialogue with institutional investors, we have received advice such as, "Why not present it from this angle?" and we have continued to refine our materials accordingly. In that sense, a positive cycle has emerged, where engagement helps us sharpen the content we disclose.

That said whether this content is truly easy to understand for all investors, including individual investors, is another matter. We recognize that there are still areas that remain difficult to grasp, such as industry specific terminology and how we communicate the credibility of our growth story, so I believe there is still room for improvement.

In the next medium term management plan, we are also considering presenting not only the growth story of our businesses, but also our purpose. In addition, when we implemented process improvements at our Indonesia operation, where expatriate staff and local employees worked together to improve manufacturing efficiency, we came to realize that the growth of people leads directly to the growth of the company. I think perspectives such as investment in human capital are also important.

Koike How about you, President Takeda of Sanoh Industrial?

Takeda We have very similar concerns to Mitsubishi Steel. Remaining in TOPIX is also one of our important management issues, and fundamentally, we need to raise our share price. If we are viewed under the "transport equipment" sector, it is difficult for us to be seen as a growth industry. We believe that self-help is essential, by clearly drawing out our equity story and continuing to deliver the results that support it.

In our existing automotive parts business, as competitors withdraw and the market becomes more concentrated, we have put forward a company specific strategy we call the "Sanoh Last Man Standing Strategy," which is essentially a strategy to capture profit of the remaining players by continuing to stay in the market until the very end, as long as customers continue to need us, and using that cash to invest in new businesses. However, investors often doubt whether we can really do both. At times, these two approaches are seen as conflicting. From our perspective, we intend to steadily accelerate early cash generation and invest the cash we create into new businesses more aggressively than ever before.

We also want to increase our opportunities for dialogue not only with domestic investors, but with overseas institutional investors as well. If we do not break away from old fashioned thinking and align both our governance and our operations with global standards, we will not be able to compete on the world stage. In that sense, feedback from overseas investors is extremely valuable to us.

The Structural Problem of Insufficient Analyst Coverage

Koike As a common issue across all your companies, it seems that analyst coverage is limited. This is especially true in the Growth Market, where even if the lead underwriter’s analyst writes a report at the time of listing, coverage is often dropped afterward.

Kozue Yes, we have almost no contact with analysts. There are no reports published either.

Sugimoto The same is true for us. This is an issue for the industry, and we are looking to strengthen our sponsored research business. This is a framework in which the issuer itself bears the cost, and a third party, such as an IR firm, produces and disseminates objective research reports.

As sell side analysts continue to decline, we believe this could become a new option for delivering company information to investors.

Koike Without analyst reports, institutional investors may not even have a first point of entry when considering an investment. When I served as Chairman of the Securities Analysts Association of Japan, insufficient coverage was also a major topic of discussion. This is a deeply rooted issue, with a historical background in which investment banking divisions reduced their research teams in order to cut costs.

I would also like to ask about your IR setup. How many dedicated IR personnel do each of your companies have?

Kozue It is two people, the CFO and one dedicated staff member.

Sugimoto Our IR function is handled by three people, the CFO, an IR officer, and me.

Yamaguchi Our IR team consists of four people, and we also work closely with our corporate planning department.

Takeda We have four or five people dedicated to it full time.

Koike Staffing really is a major issue. In particular, we often hear from Growth Market companies that they do not have dedicated IR personnel, or that they are unable to develop them internally.

Sugimoto Our clients often ask us, "Do you know anyone good?" It seems to me that there is a shortage of people who can take on IR responsibilities across the market.

The Future of the Japanese Stock Market, Shaped Through Dialogue

Koike Thank you very much for your valuable insights today. Your sense of the issues came through very clearly.

I recently spoke with a sovereign wealth fund from the Middle East, and they told me that their interest in Growth and small cap names as investment destinations in Japan is extremely strong. However, for them, funds in the range of only several tens of billions of yen are simply too small, and they end up saying, "If that is the case, we would rather go to Nasdaq in the United States." It is truly regrettable that large pools of overseas capital are not reaching Japan’s growth companies in sufficient measure, and unless we do something to break through this situation, there is no future for Japan’s capital markets.

I will make sure that the candid feedback shared today is fully reflected in the Tokyo Stock Exchange market reform follow up committee in which I participate. And I would also like to make this conversation the start of an ongoing relationship, not just a one-off exchange, so that we can continue to hear about your progress and also consult with you on new initiatives we are considering.

It is only through continuous dialogue and the exchange of ideas between companies and investors that this country’s capital markets will move forward. I am confident that today’s discussion marks an important first step. Thank you very much for today.

This article is not intended as investment solicitation, nor does it constitute a recommendation to buy or sell any specific security or imply any rise or fall in price.

(Date of publication: April 24, 2026)